An Employee Guide to 401(k) Plans

Experts say that most people will need between 70% – 85% of their pre-retirement income each year after retirement. Because many people will live more than 20 years after they retire, planning for retirement is one of the most important long-term goals you can make for yourself.

Retirement savings comes from three general sources:

- Social Security benefits

- Retirement or pension plans

- Personal savings

Why should I participate in my company’s retirement plan?

Although planning and preparing for retirement at any point in your life can be daunting, a company-sponsored retirement plan is a great way to save towards that goal.

Here are a few reasons to enroll in your company’s 401 (k) plan:

- Lower your current tax liability — Contributions to a 401(k) plan are pretax’ and will reduce your taxable income. (Earnings and/or interest on your contributions are not taxed until you take a withdrawal)

- Higher limits than other retirement plans — In 2022, you may contribute up to $20,500 to a 401 (k) plan, compared to $6,000 to a traditional or Roth IRA. If you are age 50 or older, you may contribute up to $27,000 to a 401(k), compared to $7,000 to a traditional or Roth IRA.

You can contribute to your 401 (k) plan and an IRA in the same year. Depending on your tax-filing status and your Adjusted Gross Income, your contributions to your IRA may be deductible.

- Savings made easy — Contributions to a 401(k) plan are made each pay period via payroll deductions, making saving money a piece of cake.

- Employer contributions? — Some companies fund employer contributions or match. Think of an employer contribution as additional compensation that you are automatically saving towards retirement. In addition, employer contributions and the earnings on those contributions are pretax, just like your employee contributions.

When should I start?

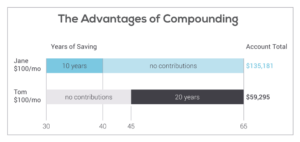

You are never too young to start saving for retirement. Actually, the earlier you start saving the better off you are for two reasons: 1. Compounding — If you start saving for retirement at an early age, even small contributions make a big difference in the long term. Your contributions generate tax-deferred earnings, which are automatically reinvested, creating a cycle where your earnings generate new earnings. Here is an example: Both Tom and Jane contribute $100 to their respective 401(k) plans. However, Jane started contributing when she was 30 years old. After 10 years, she stopped putting money into her 401(k) plan. On the other hand, Tom didn’t start saving until he was 45 years old. He contributed $100 a month until his retirement at age 65. Even though Jane saved much less than Tom, she started saving earlier and had more time for her money to compound.

I am over 40 with no retirement savings – is it too late?

It is never too late to get started saving for retirement. Take advantage of the high contribution limits in your company’s 401 (k) plan ($20,500 in 2022) and talk with a financial expert in order to develop realistic retirement goals. In addition, since pretax retirement plans were not introduced until the early 1980s, the government developed legislation that allows participants age 50 or older to contribute additional money to retirement plans as a “catch-up” contribution. For example, an employee age 50 or older can contribute up to $6,500 more to a 401 (k) in 2022 (for a total of $27,000). The catch-up contribution provision helps participants who did not have the opportunity to make pretax contributions prior to the 1980s make up for lost time.How much should I put in my retirement account?

How much to save for retirement will depend on many factors, including the age you want to retire, your annual income requirements after retirement, and other sources of retirement income you will be eligible for, including Social Security benefits. Other important factors, like your current financial obligations, could impact how much you can afford to save today. “With the continued market turbulence, I am worried about investing my savings.” There will always be ups and downs in financial markets. During these prolonged difficult market conditions, there are smart decisions you can make about how to invest your retirement savings:- Make a long-term plan and stick to it — Depending on your current age and when you plan to retire, you can have as many as 40 years of retirement savings ahead of you. Although you should evaluate the changes in the market, once you have created a long-term strategy, you should focus on the long term instead of reacting emotionally to changes in the market. Those who panic in response to market fluctuations may sell low or buy high.

- Continue to participate in your retirement account — In a turbulent market, it might be your instinct to stop contributing to your retirement plan. However, by continuing to contribute to your retirement plan, you can take advantage of dollar-cost averaging (not to mention the tax savings and potential compound interest).

- For example, if you defer $100 each pay period, you will purchase more shares when the price is low and fewer shares when the price is high, making your average share cost lower than the fund’s average market price.

- Review your asset allocation-An appropriate asset allocation, i.e., one that considers your risk tolerance and your time horizon, will help you stay on track for your long-term goals.